Stock depreciation with Odoo

Stock depreciation is how a business spreads the cost of an asset over its useful life instead of expensing it all at once. Each depreciation expense lowers the asset value on your balance sheet and appears on your income statement, following the matching principle.

This guide explains depreciation in simple terms: the main depreciation methods — straight line, declining balance, and double declining balance — how to calculate depreciation, how to build a depreciation schedule, and how Odoo records depreciation for your fixed assets automatically. Whether you manage a few capital assets or many, you will learn to calculate depreciation expense with confidence.

session

Book a free asset-setup session

See how Odoo can automate depreciation for your fixed assets — schedules, entries, and reports — in a free session with a Doodex specialist.

Book a free sessioncontents

- 01What stock depreciation is

- 02Depreciation expense and your financial statements

- 03The main depreciation methods

- 04How to calculate depreciation (straight line)

- 05Accelerated depreciation and declining balance

- 06The double declining balance method

- 07The units of production method

- 08Depreciation calculation, step by step

- 09Asset value and carrying value

- 10Building a depreciation schedule

- 11Depreciation in financial modeling

- 12How Odoo manages depreciation

- →Conclusion

What stock depreciation is

Stock depreciation — also called asset depreciation — is the accounting way to show that an asset loses value as you use it. When a business owns something it will use for more than a year, like a machine or a vehicle, you do not record the whole cost in one go. Instead, you spread that cost across the years the asset helps you earn money. In short, as the asset depreciates, a slice of its cost becomes an expense each accounting period.

This matters most for fixed assets and other long-term assets — tangible assets such as equipment, and capital assets the company expects to keep. (For intangible assets like software or patents, the same idea is called amortization.) Depreciation is a non-cash expense: no money leaves your account when you record it, yet it lowers your reported profit. Because it is a non-cash expense, it is also usually an operating expense on the books.

Depreciation expense and your financial statements

Depreciation touches two of your main financial statements. The depreciation expense for the year shows up on the income statement, where it reduces profit. At the same time, the running total — called accumulated depreciation — sits on the balance sheet and reduces the asset value shown there. The matching principle is the reason: you recognize the cost in the same period as the revenue the asset helps create.

There is a real tax benefit, too. Because depreciation is a non-cash expense, it reduces taxable income for tax purposes — depreciation reduces the profit you are taxed on, even though no cash moved. Note that book depreciation and tax depreciation can differ: for tax reporting, many countries use set rules (in the US, the MACRS system), so the depreciation amount on your tax return may not match the books. Following recognized accounting standards keeps the treatment consistent for normal accounting purposes.

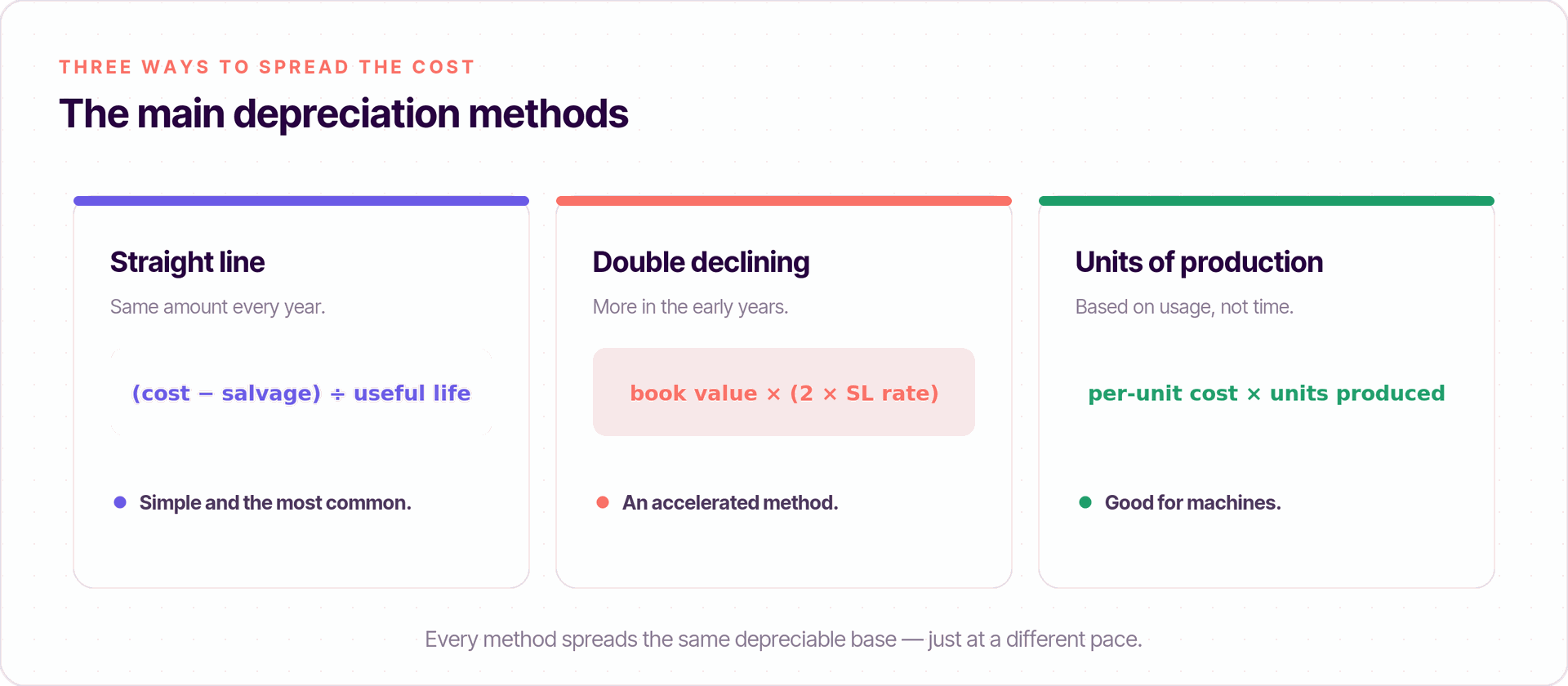

The main depreciation methods

There are a few standard depreciation methods, and they differ only in how fast they spread the cost. Three values drive every one of them: the asset's cost (its purchase price), the salvage value (what it is worth at the end), and the estimated useful life (how many years you will use it). The cost minus salvage value is the depreciable base — the part you actually spread out.

How to calculate depreciation (straight line)

The straight line depreciation method is the simplest and the most common. With the straight line method, you charge the same annual depreciation every year of the asset's life.

The straight line rate is just 1 ÷ useful life. So an asset with a five-year life depreciates at 20% a year. To calculate depreciation this way, you only need three numbers — the initial cost, the salvage value, and the number of years — which is why most teams start here. The result is a steady, predictable annual depreciation expense.

Accelerated depreciation and declining balance

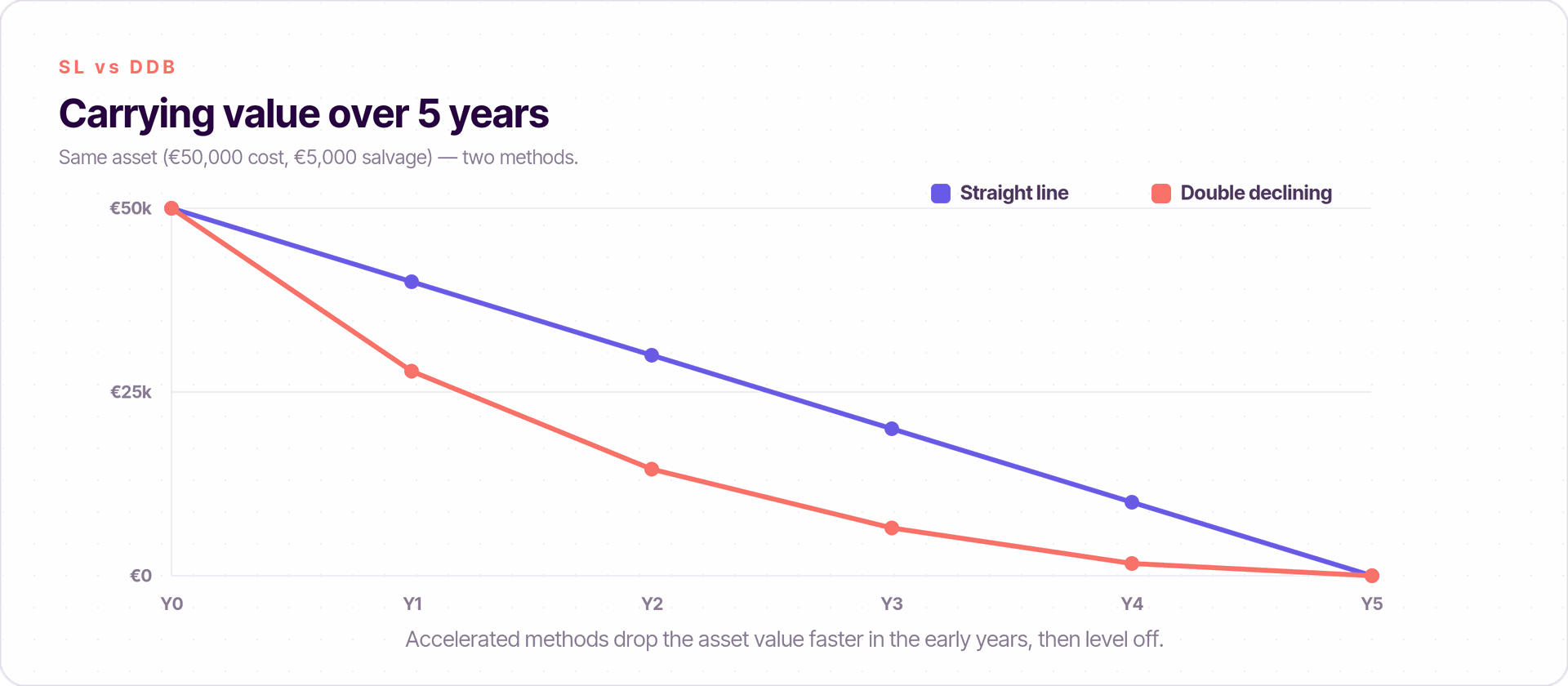

Sometimes an asset gives most of its value early — think technology assets that age fast. Accelerated depreciation matches that by charging more in the first years and less later. The declining balance approach does this by applying a fixed depreciation rate to the asset's book value (its remaining value) each year, rather than to the original cost.

Because the book value shrinks every year, each year brings lower depreciation than the one before — the asset takes less depreciation as it ages. This accelerated depreciation method is popular when you want the expense to follow how quickly the asset depreciates in the real world.

The double declining balance method

The double declining balance method is the most-used accelerated approach. As the name says, double declining balance uses twice the straight-line rate.

For a five-year asset, the straight-line rate is 20%, so the double declining balance rate is 40%. You apply 40% to the carrying value each year and stop once the book value reaches the salvage value. This front-loads the expense, which can be useful for tax purposes in the early years.

Free session

Want depreciation set up in Odoo?

Book a free working session with a Doodex Odoo specialist and get your assets, methods, and schedules configured end to end.

Book a meetingThe units of production method

The units of production method ties depreciation to use, not time. Instead of a yearly figure, you work out a cost per unit, then multiply by the units produced in the period. This production method fits machines whose wear depends on output.

It gives the truest picture for equipment, because a busy year carries more expense and a slow year carries less. Estimating total output usually relies on historical data from similar assets.

Depreciation calculation, step by step

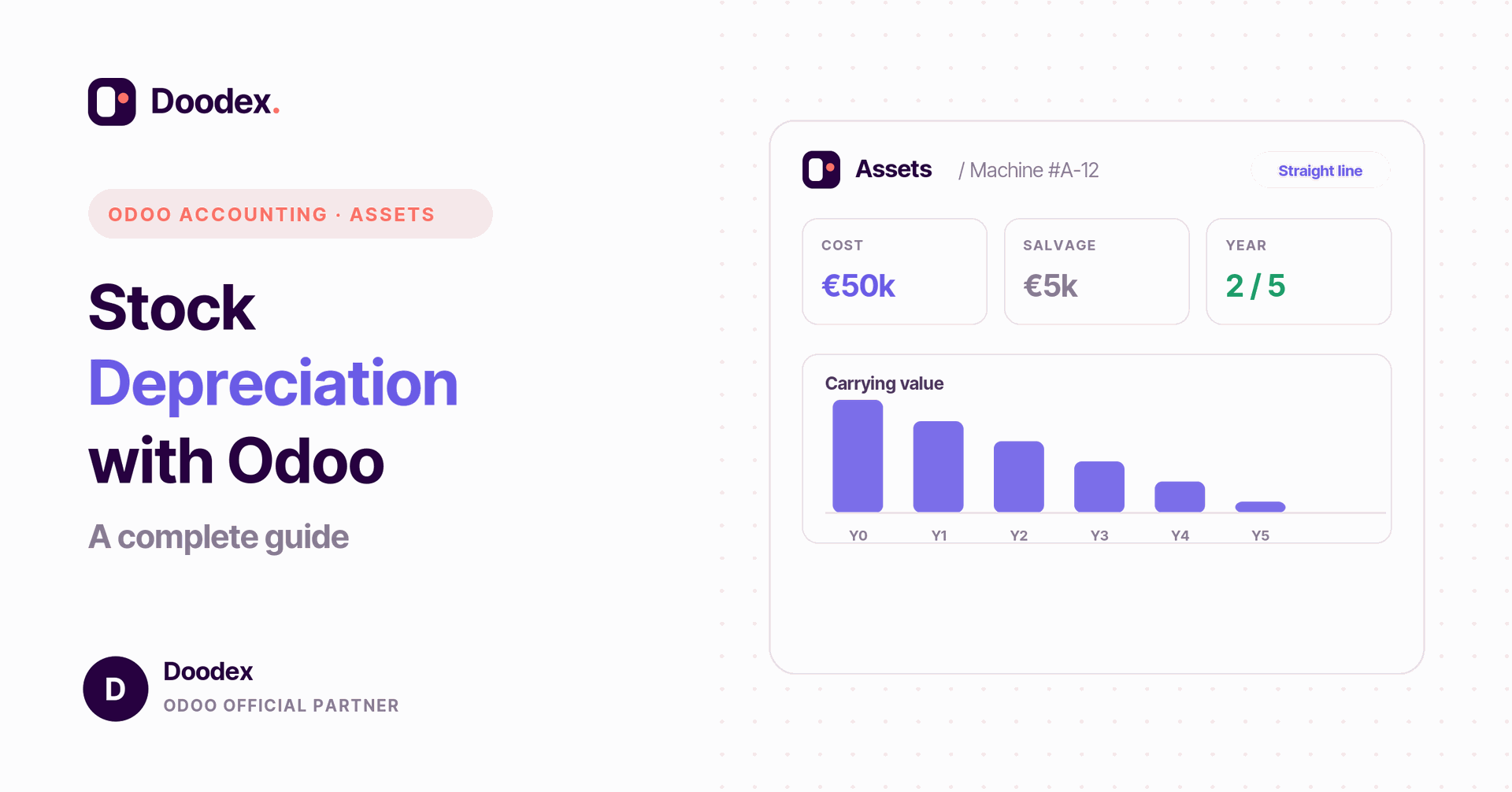

Here is the full depreciation calculation with a simple example. A company buys a machine for €50,000 (its original purchase price and total cost), expects a salvage value of €5,000, and a five-year asset's life. To calculate depreciation expense with the straight line method:

- Find the depreciable base: €50,000 − €5,000 = €45,000.

- Divide by the useful life: €45,000 ÷ 5 = €9,000 a year.

- Record €9,000 of depreciation each year until the total depreciation reaches €45,000.

That €9,000 is your annual depreciation, and over five years the total depreciation expense equals the depreciable base. The leftover €5,000 is the salvage value, which you never depreciate.

Asset value and carrying value

As you record depreciation, the asset value on the balance sheet falls. The figure shown is the carrying value — also called book value — and it equals cost minus accumulated depreciation.

This is not the same as market value, which is what you could sell the asset for today. Book value follows your accounting rules; market value follows the market. Both matter, but only the carrying value drives the numbers in your financial statements.

Building a depreciation schedule

A depreciation schedule lays out every year in one table: the depreciation expense, the accumulated depreciation, and the remaining carrying value. It is the clearest way to see how an asset depreciates over its life. Here is the straight-line schedule for our €50,000 machine:

Each year the carrying value is carried forward to the next row. A schedule like this is what you use to record depreciation in the books and to plan ahead.

Depreciation in financial modeling

Depreciation is a key line in financial modeling. Because it is predictable, analysts use the depreciation schedule to forecast future profit and cash flow, and to plan capital expenditures (capex) — the spending on new capital investment. Models often split this into growth capex (new capacity) and maintenance capex (keeping current assets running), using historical data as a guide.

The scale can be large: publicly traded companies report big numbers here — for example, Coca-Cola reported depreciation and amortization of about $1.1 billion in 2023. Whatever the size, the same logic applies, and a clean schedule keeps the accounting treatment consistent.

How Odoo manages depreciation

Odoo's Accounting app handles all of this for you through its Assets feature. You enter the asset once — its purchase price, salvage value, useful life, and the method (straight line, declining, or declining-then-straight-line) — and Odoo builds the full depreciation schedule automatically.

- Automatic entries. Odoo posts each depreciation expense on the right date, so the income statement and balance sheet stay accurate with no manual work.

- Live asset value. The carrying value updates as depreciation runs, so the asset value on your books is always current.

- Any method. Pick the straight line method for steady cost or an accelerated method for front-loaded expense.

- Reports. See total depreciation, remaining value, and a depreciation schedule for every asset, plus data you can reuse for financial modeling.

Because the Assets feature is linked to the rest of Accounting, recording depreciation needs no double entry — the journal entries, the financial statements, and the depreciation amount all stay in sync. At Doodex, we set this up so your fixed assets manage themselves.

Conclusion

Stock depreciation turns a big one-time cost into a fair yearly expense that matches how an asset is used. Once you know the three inputs — cost, salvage value, and useful life — you can calculate depreciation with any method, build a clear depreciation schedule, and see the effect on your income statement and balance sheet. Pick the method that fits the asset, keep the schedule current, and your financial statements will always tell the truth.

Odoo makes the whole process automatic, from the first entry to the final depreciation amount. If you want help setting up depreciation and asset management for your business, Doodex can do it for you.

Your Odoo partner

Want automatic asset management?

Doodex sets up Odoo asset management and depreciation end to end - from the first entry to reports your accountant will love. Talk to our team to get started.

Talk to a Doodex expertanswered

What is stock depreciation in one sentence?

It is spreading the cost of an asset across its useful life as a yearly depreciation expense, instead of expensing it all at once.

Which depreciation method should I use?

Use the straight line method for steady, simple costs; use an accelerated method like double declining balance when an asset loses value fast; use units of production when wear depends on output.

How does depreciation affect taxes?

Depreciation is a non-cash expense that reduces taxable income, so it lowers the profit you are taxed on — though tax reporting rules can differ from your book figures.

What is the difference between book value and market value?

Carrying value (book value) is cost minus accumulated depreciation on your books; market value is what the asset would sell for today.